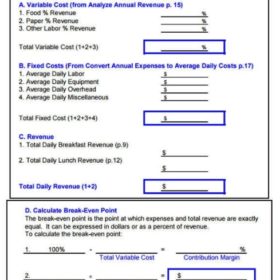

A break-even analysis template is a tool which is actually a point at reaching company break-even. Generally, this analysis will help businesses to prepare this tool for different reasons and expansions. Thus, a break-even analysis is used to calculate what is known as a margin of safety, where the earned profit is equal to investment and the business can prove very athletic. It is helpful for deciding whether to make a purchase before reaching the level of break-even or not. Here people can use variables to compute a break-even analysis. In addition, the actual amount that revenues exceed the break-even is noted as a point of break-even, although the amount that revenues can fall will stay above the break-even point.

Assumption and Limitation of Break Even Analysis:

A break-even analysis template has great importance and is very useful not only for professionals but also for young individuals. Every passing day, this tool is being accepted by people around the globe as a great help to improve their businesses. Nevertheless, like any other analysis tool, it also has some limitations and assumptions. Here underneath we shall try to elaborate on each and every point clearly, for your ease. These points are given below:

Assumption of Break Even Analysis:

The following points are some of the common assumptions of this tool and these are given below:

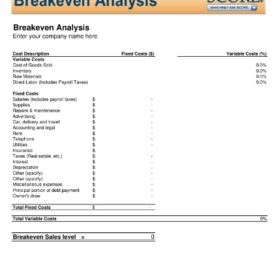

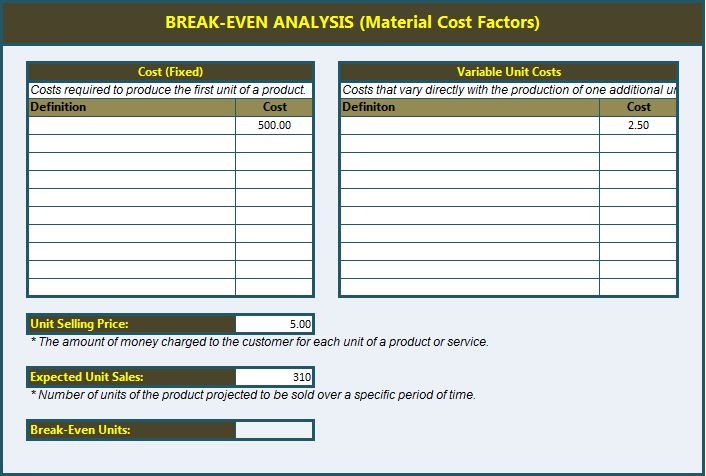

Types of Costs: There are two types of cost of any project or business; fixed cost and variable cost. A fixed cost remains fixed throughout the life of the project. Whereas, variable cost remains variable depending on different elements.

Earnings: Earnings are the source from which investment cost is recovered or balanced. It will continue to flow until business activities are ceased. Its trend can be seen upwards and downwards throughout the life of business.

Sales Price: A sales price is the cost which consists of total cost plus profit. A sales price per unit can be obtained from books of account to determine the amount of earnings.

Volume or Number of Units Sold: Total amount which can be recovered in the shape of earnings will remain unchanged until total earnings crossed initial investment.

Extra Ordinary Events: No special event can change or alter fixed, and variable cost expect extraordinary events, which must be expressed in writing. Sales price as per calculated should remain unchanged.

Other Factors Remain Same: All other factors which are considered in analysis will remain the same. These are technology, equipment, production methods and working efficiency.

Inventory: There are no opening balance and ending balance of inventory. Whereas, inventory quantity will also remain the same and unchanged.

You can check our Problem Analysis Example.

Limitations of Break Even Analysis:

1. Output Cost: Based on analysis, inventory will remain the same but as production increases, output cost will also increase, which is ignored in this method.

2. Change in Cost Amount: Fixed cost and production cost remain the same, whereas it is not possible due to production errors and breaks. The fixed cost per unit can remain the same, but variable cost per unit can change with the passage of time. This assumption is not valid in this method.

3. Output Levels: Sales cost and variable cost both may variate as production increases or decreases, and it is not assumed properly.

4. inflation: Inflation rate is not considered in the calculation and that makes its assumption non-workable. Inflation rate is part of external factors which are considered unchanged.

5. Production Methods: Change in technology can provide more economical methods of production which are ignored in this tool. Production costs vary from each production level and this is also ignored while computing break-even analysis.

Importance of Break Even Analysis:

While living in the modern world of business, if you’re running a company or brand, then obviously you’ll always find a familiar tool for tracking the cash flow of your company professionally. Well, here in this article we’ll talk about break-even analysis. Basically, a break-even analysis is a scientific term which is pretty much useful for calculating the cash flow. However, this analysis will be conducted as a fairly simple calculation where you can determine whether a solid point at which your company receives revenue equals the costs those thoroughly associated with the receiving revenues. Moreover, as we can assume that there is always a point reaching on it, the company becomes a profitable enterprise.